-

Complete Solaria Reports Third Quarter 2023 Results

Источник: Nasdaq GlobeNewswire / 14 ноя 2023 18:27:07 America/New_York

FREMONT, Calif., Nov. 14, 2023 (GLOBE NEWSWIRE) -- Complete Solaria Inc. (NASDAQ: CSLR) published its third quarter 2023 results, which will be reviewed for investors at 5:00 p.m. EST today at https://investors.completesolaria.com/.

Third quarter summary (financial comments based on non-GAAP results unless noted):

- Revenue (systems only) of $24.6 million, down 4% from previous quarter

- Modules sales, $3.8 million, reported as “discontinued operations,” not revenue

- 25% gross margin, up from 18% in the prior quarter

- Sale of Module business and transfer of 26 employees to Maxeon for $10.2 million

- Leaning out the company: second RIF of 68 with $7.5 million of annualized savings

- Systems bookings remained strong with $56.4 million in new contracts, a record

Fellow Shareholders:

Our revenue and earnings for Q3 2023 are given below, compared with Q2 2023 actual results and a Q4 2023E forecast:($1000s, except gross margin) GAAP Non-GAAP1 Q3 2023 Q2 2023 Q3 2023 Q2 2023 Q4 2023E3 Revenue 24,590 32,173 24,590 32,173 22,000 Gross Margin 25% 17% 25% 18% 35% Operating Income (11,078) (17,546) (9,231) (15,788) (5,698) Cash Flow2 (884) (804) (884) (804) 973 Cash Balance 1,661 2,545 1,661 2,545 2,634 1. Reconciliation to GAAP attached.

2. Includes funding of $10,252 in Q2 (deSPAC bridge), $19,500 in Q3 (deSPAC) and $10,153 in Q4 (Maxeon).

3. Ranges: $21-$23M revenue, 32%-40% GM, ($4)-($8)M opinc, $1M cash flow (minimum), $1M end cash (minimum), based on agreement with current shareholders.Chairman’s Report

A Systems Company

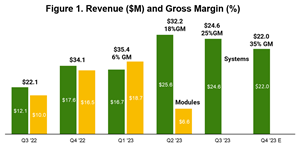

We have completed the Module business divestiture to Maxeon and received $10.2 million, which provides the cash needed in our Q4 plan. This restructuring and singular focus on our high-margin systems business model raised our gross margin to 25% in Q2, and we aim to further improve it to the 32%-40% range in the current Q4 quarter.Figure 1 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/e3ade911-f53e-44c2-8953-91dbca423034

Reducing Excess Fab Inventory

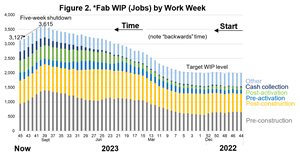

Our Q3 revenue was $24.6 million, below the “above $30 million” revenue expectation I wrote in the Q2 report and the $38-$41 million previous street expectation. The fab remained overloaded because our incorrect assumption that the improvements we made allowed us to load the line with all the contracts we received during Q3, but that bloated the fab WIP to 3,615 jobs as is shown in the WW39 WIP inventory graph below. I consequently shut down new starts in the fab for five weeks, and the excess inventory dropped by 13.5% to 3,127 jobs.Figure 2 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/f6ba9cf4-12b0-42cc-82f7-69e49af1182a

Plan to Achieve Cash Flow Breakeven & Profitability

We now have a growing company with $88 million in annualized revenue that comes solely from the high-margin systems business. Our plan is to make that $88 million in revenue profitable as soon as possible by leaning out the organization further and increasing its efficiency using classic quality control methods. Paradoxically, our increase in orders into the line in Q3 slowed the fab down and thus again impeded revenue growth. Our plan after the five-week shutdown is to limit fab starts this quarter to produce $22 million in revenue in Q4 – and focus our engineering and operations efforts on making that $22 million more profitably, and with better quality. While it does not yet show up on the bottom line, we did make significant progress in the third quarter on our “North Star” plan to achieve profitability and cash flow independence in 2024.The North Star plan simultaneously drives three key components of profitability: 1) reducing opex from $12,875 (all numbers in $1000s) in Q2 to $6,732 in Q3 (done) and then to our $5,918 forecast for Q4 (on track), 2) reducing our sales commissions from 36% in Q3 to 34% in Q4 and 32% in Q1, and 3) increasing gross margin from 18% in Q2 to 25% in Q3 (done) and again to 32%-40% in Q4 (on track). We have made significant progress on each North Star component, as detailed below.

Leaning Out The Organization

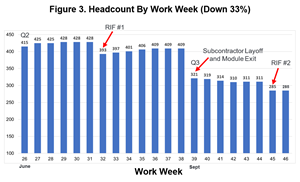

As shown in the headcount graph below, by the end of the second quarter (WW26), our headcount had been reduced to 415. In Q3 (WW39), two more RIFs reduced our headcount further to 321 in Q3, saving an incremental $10.6 million annually. Today (WW46), our headcount is down 33% to 285 and will be lower yet by the end of the quarter. And – as is typical – when the lean method is used, our performance has actually improved with fewer people.Figure 3 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/a9a3024b-649b-4b7e-ba9b-d678b80812f8

When our headcount reduction is combined with other cost reductions, opex was reduced from $12,875 in Q2 to $6,732 in Q3 (done), and we are on track to reduce opex to $5,918 in Q4.

Conclusion

Although our bottom line does not yet show it, we have made major progress in quality and our North Star profitability goals by restructuring to a systems-only company, reducing headcount by 33%, reducing our panel cost from an average cost of $0.61/watt with our new $0.25/watt contract, and our commissions from 34% as we phase in our new 30% rate. We expect these improvements to cut our operating income losses from $15.8 million in Q2 to $9.2 million in Q3 (done) and to $5.7 million in Q4. The profit improvement will improve cashflow losses in Q4 to levels already funded by the Maxeon divestiture. Our planned future cash need is less than $5 million in total cashflow needed until mid-2024. Obviously, these estimates have high uncertainty in a company with immature business processes in the current chaotic market, but the company has become fundable by existing investors with acceptable dilution.We have established a franchise with $88 million in annualized revenue. We will build shareholder value by driving CSLR to operating profitability, which we can credibly envision for the first time.

Building The Complete Solaria Team

We have a new CEO: Taner Ozcelik. Founder Will Anderson will report to him.

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/6a2c4993-82bf-4f18-9cc6-4089cfb6d0f8

Born in Turkey

#82 among 650,000 college entry students, country-wide

Bronze metal at World Mathematics Olympiad, Helsinki

23 US patents, 12 technical papers

MBA, Wharton

PhD Electrical Engineering, Northwestern. GPA 3.9/4.0

Sony, ’95-’01: founded semiconductor unit, grew it from $0-$200 million

Nvidia, ’04-’14: founded automotive semiconductor unit, grew it from $0-$600 millionLaunched Tegra AI supercomputer chip for autonomous driving

Designed Tegra into 126 cars at 23 companies

Car of the year awards: Tesla Model S, Audi A3On Semi: ’14-’21, 800 employees, 13 countries, $250M budget

Grew Smart Sensor division from $590 million to $850 million

Fixed “distress asset” Cypress imaging divisionAnd, we have a new board member: Chris Lundell

A photo accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/20c7e5ba-c096-4993-8b95-00548179a595

Brigham Young, MBA, 3.85 GPA, Finance & Economics

Novel, 1990-2003: Five promos ending as VP of Marketing

Vivint Solar: ’13-’16, CMO at Vivint 2013 for their IPO

CMO Grow: CEO of a national consulting company that creates scalable growth plans

Lives in Salt Lake near our main plant; connected to Salt Lake “Solar Valley”CEO’s Report

Continued Strong Customer Demand

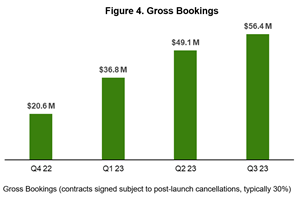

While our industry has reported slowing customer demand, Complete Solaria has experienced the opposite. In the third quarter the Company experienced record gross bookings of $56.4 million, a 1.4x increase over the same period last year.Figure 4 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/a3c97809-c663-4fd0-a478-a9f55b2b6f0b

Complete Solaria’s two most important core competencies have always been: 1) We make selling solar easy, and 2) we deliver a fast, world-class customer experience. The increase in new bookings – even in markets like California that are experiencing regulatory headwinds – proves that our model effectively drives customer demand.

Improving the Fab

We have made progress in reducing the excess inventory in our fab, the primary cause of project delays. These delays come from both external factors such as long permitting and utility approval cycles, but primarily from internal factors such as quality of execution and difficulty in scaling our corporate business processes rapidly to beyond the $88 million revenue level we are at. The compounding effect of record new orders and delayed project completions resulted in significant wait times for many customers and a reduction in customer satisfaction, which improved in Q3 but has not yet returned to historical levels.To improve the customer experience, we need to further reduce fab WIP by limiting the number of new projects we launch into the fab. Specific actions we have taken to accomplish this include:

- Shutting down new order launches for five weeks during Q3 to kick-start fab WIP reduction.

- Establishing a Quality Department led by an experienced VP Quality. The department is responsible for reducing rework and defects that slow down our business processes. It has defined and implemented strict quality gates at project launch to control WIP and to avoid installation errors. This is the main reason we are throttling our revenue to $22 million in Q4.

- Hiring a VP IT to increase the scalability of our IT systems.

- Extending the engagements of senior consultants in IT, fab management, quality and customer service management to help us scale more quickly.

These actions have already resulted in a significant reduction of our fab inventory as shown. However, there are still many aged projects in our fab, which will flush out over the next two quarters, during which we will return to our faster historical cycle times.

Improving Gross Margin

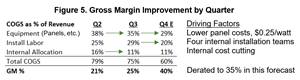

We improved gross margin from 18% in Q2 to 25% in Q3. The primary contributors to the improvement in Q3 were reductions in the cost of solar modules and other equipment and reduced headcount. These gains were partially offset by an increase in installation labor, especially in the Northeastern US. We invested in four internal installation teams which will provide lower Q4 installation costs. Our “GM47” project, which I personally run, is targeted to add ten percentage points to our Q3 GM of 25% this quarter, as quantified below:Figure 5 is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/feb535d7-075a-40f4-b265-8b3269c05fea

We are targeting 32%-40% Q4 gross margin as driven by lower solar panel, inverter, and battery pricing, as well as the benefits of using lower-cost internal installation teams.

Conclusion

Complete Solaria now focuses solely on what it does best – the Systems business. We are striving to regain our prior performance in rapid fulfilment and customer satisfaction. Investors will see a steady improvement in our financial metrics.About Complete Solaria

Complete Solaria is a solar company with unique technology and an end-to-end customer offering – which includes financing, design and project fulfilment, and follow-on customer service – allowing it to sell more products across more markets and enable more options for customers wishing to make the switch to a more energy-efficient lifestyle. To learn more, visit https://www.completesolaria.com.Forward Looking Statements

This press release contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, about us and our industry that involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “will,” “goal,” “prioritize,” “plan,” “target,” “expect,” “focus,” “look forward,” “opportunity,” “believe,” “estimate,” “continue,” “anticipate,” and “pursue” or the negative of these terms or similar expressions. Actual results could differ materially from these forward-looking statements as a result of certain risks and uncertainties. For additional information on these risks and uncertainties and other potential factors that could affect our business and financial results or cause actual results to differ from the results predicted, readers should carefully consider the foregoing factors and the other risks and uncertainties described in the “Risk Factors” section of the registration statement on Form S-4 filed, which was declared effective by the Securities and Exchange Commission (the “SEC”) on June 30, 2023. Such filings identify and address other important risks and uncertainties that could cause actual events and results to differ materially from those contained in the forward-looking statements. Forward-looking statements speak only as of the date they are made. Readers are cautioned not to put undue reliance on forward-looking statements, and Complete Solaria assumes no obligation and does not intend to update or revise these forward-looking statements, whether as a result of new information, future events, or otherwise.Contacts: Brian Wuebbels

CFO

bwuebbels@completesolaria.comSioban Hickie

Investor Relations

CompleteSolariaIR@icrinc.comComplete Solaria, Inc. Condensed Consolidated Balance Sheets (Unaudited) (In Thousands, Except Share and per Share Amounts) October 01,

2023December 31,

2022Assets Current Assets: Cash $ 1,661 $ 4,409 Accounts receivable, net 26,003 27,717 Inventories, net 12,503 13,059 Prepaid expenses and other current assets 9,947 10,071 Total Current Assets 50,114 55,256 Property, plant and equipment, net 4,185 3,476 Long-term assets held for sale - discontinued operations 12,299 162,032 Other assets 5,421 7,419 Total Assets $ 72,019 $ 228,183 Liabilities and Stockholders' Equity Current Liabilities: Accounts payable $ 14,571 $ 14,474 Accrued expenses and other current liabilities 35,681 25,237 Notes payable and short-term debt 57,128 20,403 Total Current Liabilities 107,380 60,114 Redeemable convertible preferred stock warrant liability 10,240 14,152 Long term debt and convertible notes - 44,148 Other long term liabilities 5,182 4,488 Total liabilities 122,802 122,902 Stockholders' deficit (50,783 ) 105,281 Total liabilities, mezzanine equity and stockholder' deficit $ 72,019 $ 228,183 Complete Solaria, Inc. Condensed Consolidated Statement of Operations (Unaudited) (In Thousands, Except Share and per Share Amounts) 13 weeks

endedQuarter

Ended39 weeks

endedNine months

endedOctober 1,

2023September

30, 2022October 1,

2023September

30, 2022Revenues $ 24,590 $ 12,260 $ 66,887 $ 48,974 Costs revenues 18,354 8,266 51,788 33,792 Gross profit 6,236 3,994 15,099 15,182 Operating expenses: Sales commissions 8,755 3,572 23,221 15,694 Sales and marketing 2,214 1,604 5,216 4,607 General and administrative 6,345 2,027 22,965 6,194 Operating expenses 17,314 7,203 51,402 26,495 Loss from continuing operations (11,078 ) (3,209 ) (36,303 ) (11,313 ) Other income (expense), net (39,896 ) (937 ) (37,146 ) 508 Loss before income taxes (50,974 ) (4,146 ) (73,449 ) (10,805 ) Income tax provision 1 - 1 (4 ) Net loss from continuing operations $ (50,973 ) $ (4,146 ) $ (73,448 ) $ (10,809 ) Discontinued operations Loss from discontinued operations, net of tax (8,404 ) - (20,953 ) - Impairment loss from discontinued operations (147,505 ) - (147,505 ) - Net loss from discontinued operations (155,909 ) - (168,458 ) - Net Loss $ (206,882 ) $ (4,146 ) $ (241,906 ) $ (10,809 ) Comprehensive income (loss) Foreign currency translation adjustment 10 - 24 - Comprehensive income (net of tax) (206,872 ) (4,146 ) (241,882 ) (10,809 ) Net loss per share from continuing operations, basic and diluted $ (1.28 ) $ (0.31 ) $ (4.33 ) $ (0.83 ) Net loss per share from discontinued operations, basic and diluted $ (3.92 ) - (9.92 ) - Net loss per share, basic and diluted $ (5.20 ) $ (0.31 ) $ (14.25 ) $ (0.83 ) Weighted average number of common shares outstanding, basic and diluted 39,821,078 13,431,410 16,973,195 13,053,367 Complete Solaria, Inc. RECONCILIATION OF NON-GAAP FINANCIAL MEASURES (In Thousands) 13 weeks

endedQuarter Ended 39 weeks

endedNine months

endedOctober 1,

2023September 30,

2022September 30,

2023September 30,

2022GAAP operating loss from continuing operations Note (11,078 ) (3,209 ) (36,303 ) (11,313 ) Stock based compensation A 1,630 85 2,321 217 Transaction related charges B - - 2,765 - Restructuring charges C 217 - 217 - Total of Non-GAAP adjustments 1,847 85 5,303 217 Non-GAAP net loss (9,231 ) (3,124 ) (31,000 ) (11,096 ) Notes: (A) Stock-based compensation: Stock-based compensation relates primarily to our equity incentive awards. Stock-based compensation is a non-cash expense. (B) Transaction related charges: These expenses are related to audit and consulting fees in connection with efforts needed for the DPAC process, which includes IPO readiness, catch-up audits etc. (C) Change in fair value of warrants: this is a non-cash, non-operating impact. Complete Solaria, Inc. Non-GAAP Condensed Consolidated Statement of Operations (Unaudited) (In Thousands, Except Share and per Share Amounts) 13 weeks

endedOctober 1,

2023Revenues $ 24,590 Costs revenues 18,334 Gross profit 6,256 Operating expenses: Sales commissions 8,755 Sales and marketing 2,019 General and administrative 4,713 Operating expenses 15,487 Loss from continuing operations (9,231 ) Other income (expense), net (1,987 ) Loss before income taxes (11,218 ) Income tax provision 1 Net loss from continuing operations $ (11,217 ) Net loss per share, basic and diluted $ (0.28 ) Weighted average number of common shares outstanding, basic and diluted 39,821,078 Use of Non-GAAP Financial Measures

Non-GAAP gross margin, non-GAAP operating income and other non-GAAP measures are intended as supplemental financial measures of our performance that are neither required by, nor presented in accordance with GAAP. We believe that the use of Non-GAAP measures provides an additional tool for investors to use in evaluating ongoing operating results, trends, and in comparing our financial measures with those of comparable companies, which may present similar Non-GAAP financial measures to investors.

However, you should be aware that when evaluating the non-GAAP measures, we may incur future expenses similar to those excluded when calculating these measures. In addition, the presentation of these measures should not be construed as an inference that our future results will be unaffected by unusual or nonrecurring items. Our computation of non-GAAP gross margin, non-GAAP operating income and other non-GAAP measures may not be comparable to other similarly titled measures computed by other companies, because all companies may not calculate the non-GAAP measures in the same fashion.

Figure 1

Revenue ($M) and Gross Margin (%)

Figure 2

*Fab WIP (Jobs) by Work Week

Figure 3

Headcount By Work Week (Down 33%)

Figure 4

Gross Bookings

Figure 5

Gross Margin Improvement by Quarter

Taner Ozcelik

Taner Ozcelik

Chris Lundell

Chris Lundell